Three decades of liberalisation: Banking highs and lows

Both the body and the soul of the industry have changed. The sellers’ market of the 1990s has become a buyers’ market. From addressing the cycle of life, the lifestyle of the customers is on banks’ radar now.

The liberalisation of India’s banking sector started soon after the opening up of the economy, with the release of the first Narasimham Committee report in December 1991. Then finance minister Manmohan Singh appointed the committee on 14 August 1991, chaired by M Narasimham, the 13th governor of the Reserve Bank of India (RBI). Yet another committee, headed by Narasimham, was appointed by another finance minister, P Chidambaram, in December 1997.

")

These two seminal reports laid the road map for the Indian banking industry — still work in progress.

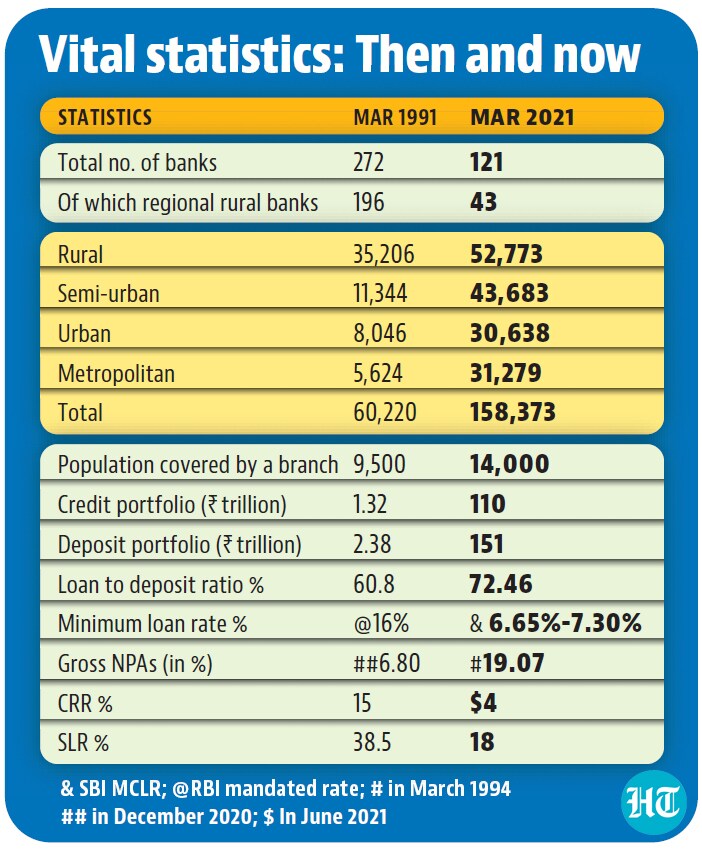

Let’s first take a look at how banking numbers stack up since 1991.

In March I991, there were 272 scheduled commercial banks in India. By March 2021, the number was 121. There were 60,220 bank branches across India in 1991 – 35,206 rural, 11,334 semi-urban, 8,046 urban and 5,624 metropolitan. By 2021, the branch network has expanded to 158,373. The growth in the rural branches has been the least (to 52,773) but the branches in other segments have grown substantially. In semi-urban areas, the number grew almost four times to 43,683; in urban pockets too, by close to four times to 30,638; and metropolitan India now has 31,279 branches. One branch now covers roughly 9,500 people, down from 14,000 in 1991.

In 1991, the deposit portfolio of the banking system was ₹2.38 trillion; and credit portfolio ₹1.32 trillion. By March 2021, the deposit portfolio was over ₹151 trillion and credit portfolio, close to ₹110 trillion.

The first Narasimham report was the springboard for the initial banking reforms – deregulation of interest rates, end of directed credit, reduction of statutory pre-emptions and the entry of new banks. The so-called cash reserve ratio (CRR) or the portion of deposits that commercial banks keep with the central bank (on which they don’t earn any interest) was 15% in 1991. Now, it is 4%. Similarly, the banks needed to buy government bonds and maintain a statutory liquidity ratio (SLR) of 38.5% in 1991. Both sucked out 53.5% of their deposits. Now, the comparable figure is 22% (4% CRR plus 18% SLR). For these reasons, the credit-deposit ratio was just 60.8% in 1991. This has risen to 72.46% after 30 years.

The minimum loan rate, prescribed by the regulator, was 16% in 1991.

In a free market, the current marginal cost of funds-based lending rate (MCLR), the floor rate for bank loans, ranges between 6.65% and 7.30% for State Bank of India (SBI), depending on the tenure of loans. For HDFC Bank Ltd, it ranges between 6.85% and 7.4%.

The key to the business of banking is the quality of loan assets. The definition of non-performing assets and loan restructuring are dynamic phenomena. Following the Narasimham Committee recommendations, a structured framework was put in place in the early 1990s, after the introduction of income recognition and asset classification norms. Initially, this framework was meant only for restructuring industrial accounts. In 2008, its scope widened to deal with stressed non-industrial accounts. By 1994, the gross NPAs of all scheduled banks were estimated to be 19.07% of all assets; for public sector banks it was even worse with 24.8%. It took more than a decade to reduce those NPAs. Falling interest rates in 21st century allowed banks to book huge treasury profits; they used surpluses to provide for bad loans.

RBI started tightening definitions of bad assets — classified sub-standard, doubtful and loss assets — early this century but the prudential norms were held hostage by government policies. PSBs held the bulk of the NPAs but since the government did not have the money to recapitalise them, the thrust was on forbearance. Infrastructure was the holy cow in the first decade of the century. There were many incentives, including a regulatory cushion, to lend to infrastructure. These loans were also continuously restructured, and enjoyed the standard tag.

Sensing that too long a rope had been given to the banks for managing their loan books, Raghuram Rajan, who took over as RBI governor in September 2013, decided to tighten the screws. Instead of cleaning up their balance sheets, many banks indulged in what Rajan described as “pretend and extend”. They pretended that everything was fine and extended fresh loans to keep the books clean.

To address this, the Central Repository of Information on Large Credits was set up in 2014. Once the banks started supplying data in real time for all loans of ₹5 crore and above, RBI found how growth-hungry banks were giving loans to large corporations even though their balance sheets did not justify such risk-taking. No bank wanted to miss out on the credit growth story. Between 2006 and 2008, bank credit grew at a scorching pace. It dipped after the global financial crisis but picked up again in 2011.

Once RBI was convinced that the banks were camouflaging NPAs through fresh loans and other innovations, it launched the asset quality review or AQR, a first-of-its-kind health check of Indian banking, in 2015. The banks were given six quarters from October–December 2015 to January–March 2017 to clean up the mess.

Before the exercise ended, there was a change of guard at RBI but the new boss Urjit Patel carried on the clean-up exercise with greater zeal. The gross NPAs of the banking sector, which rose to 11.2% in financial year 2018, dropped to 6.8% by December 2020. It is set to rise again because of the Covid pandemic, but that’s a separate story. The Narasimham Committee made certain other critical recommendations. For instance, it said the number of public sector banks should be reduced. There could be three to four big banks; eight to ten banks with nationwide presence; and smaller regional banks. PSBs should enjoy autonomy and the era of dual control, between RBI and the banking division of the finance ministry, should give up to the ghost.

Following the consolidation drive by the government, the number of PSBs has shrunk from 27 in 2017 to 12 now. Seven of them are fairly large and at least one, SBI, is among the top 50 banks by assets, globally. The industry also welcomed new private banks in three phases – in early 1990s, early this century and in 2015. They are universal banks. While the concept of local area banks hasn’t worked out, two sets of new banks have made entry into the turf -- small finance banks and payments banks. Banking licences are now available on tap.

Autonomy for public sector banks is still a far cry even though the government has taken many steps to make them independent. Shortly after a unique offsite of the CEOs of PSBs and financial institutions, Gyan Sangyam, presided over by Prime Minister Narendra Modi and then finance minister Arun Jaitley in January 2015, the finance ministry assured all PSBs freedom from interference by the government on commercial decisions, transfers, and postings, etc.

It has also set made the selection process of CEOs of government-owned banks transparent by setting up the Banks Board Bureau -- an offshoot of the Indradhanush framework for transforming PSBs announced in August 2015. Describing this as “the most comprehensive reform effort undertaken since banking nationalization in 1970”, a government note says, “Our PSBs are now ready to compete and flourish in a fast-evolving financial services landscape.”

However, there aren’t too many takers for this optimism. At the 2015 Gyan Sangam, Modi said banks would be run professionally and there would be no interference. He added that he was against political interference but not political intervention in the interest of the people. Such political intervention, according to him, would enable the voice of the common man to reach such institutions. This has been the story of India’s public sector banking industry all along.

PSBs are political animals – the government’s milch cow, used for everything from funding infrastructure to supporting MSMEs; opening millions of zero-balance accounts for financial inclusion; buying government bonds to bridging the fiscal deficit; and subscribing to electoral bonds to help political parties.

As we complete three decades of economic liberalisation, many are crystal ball gazing on the future of PSBs: In what form and shape should they be allowed to function? How many of them should exist? The government wants to privatise at least two of them. Let’s wait and watch. Their presence is a must to address market failures and for financial inclusion and MSME- and infrastructure-financing but we don’t need all of them.

Indeed, consolidation has reduced the number of PSBs but not the government’s share in the banking industry. The problem is not with the ownership but with how the owner behaves.

This is why even before any PSB is privatised, privatisation by stealth has already started. In the 1990s, before RBI gave licences to the first set of private banks to open shop, PSBs held 90% share of the banking market. In 2000, their share was a little over 80%. Now, they are much less than 60%. PSBs’ share in incremental banking business is far lower -- even in collection of deposits, despite the sovereign backing.

That tells the story of Indian banking since economic liberalisation.

Both the body and the soul of the industry have changed. The sellers’ market of the 1990s has become a buyers’ market. From addressing the cycle of life, the lifestyle of the customers is on banks’ radar now. Beyond meeting the financial needs, they are becoming a marketplace for everything one wants.

Those banks which are changing in sync with time will survive and flourish. Others that cannot change may survive with the government’s largesse (read: recapitalisation) but the customers won’t care for them.

(The writer is an author and consulting editor Business Standard. His latest book is `Pandemonium: The Great Indian Banking Tragedy)

Get Current Updates on India News, Lok Sabha Election 2024 live, Elections 2024, Election 2024 Date along with Latest News and Top Headlines from India and around the world.